2 April 2026

Insurance is an important tool to address protection gaps. Consequently, understanding who has insurance and who does not is central to this effort.

Across many countries, individuals, families, businesses, and governments remain financially exposed to risks such as natural disasters, health shocks, and economic disruptions. Insurance plays an important role to help manage these risks, yet the extent of individual-level insurance coverage is often difficult to measure.

Across Asia's developing insurance markets, new data provide opportunities to investigate this issue. The recently released Findex Data set[1] has, for the first time, added a useful question on insurance that allowed for deeper insights.

Using this dataset, we conducted a preliminary analysis across several Asian jurisdictions to better understand patterns of insurance ownership. The findings highlight both the scale of existing protection gaps and opportunities to expand inclusive insurance solutions.

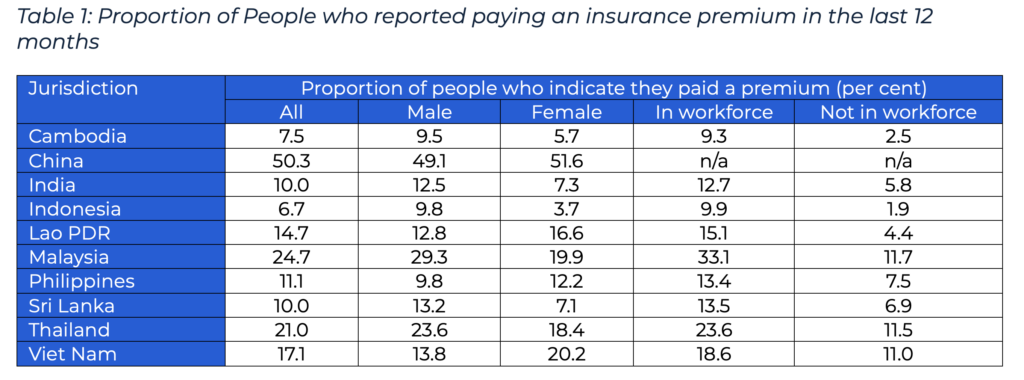

Insurance ownership varies significantly across countries

There is considerable variation in the proportion of people who report having paid for insurance. China stands out as the highest of the countries included by far. Other countries have completely unserved populations of at least 75%, and some over 90%. It is inconceivable that these unserved populations have no insurance needs at all or that the industry could not find solutions to some of those needs. Rather, the data highlights the scale of the challenges in expanding insurance access to individuals and families.

Additionally, paying a premium means that a person has some insurance. It does not mean they have all that they want or need, or that it is fully effective compared to their risks.

Men are more likely to report insurance premium payments in Cambodia, India, Indonesia, Malaysia, Sri Lanka and Thailand. In stark contrast, China, Lao PDR, the Philippines, and Viet Nam all report stronger premium payments from female respondents. Whilst there may be some explanation in the commonality of political systems between China, Lao and Viet Nam, this would make the Philippines an outlier compared to the other jurisdictions where male responses were higher.

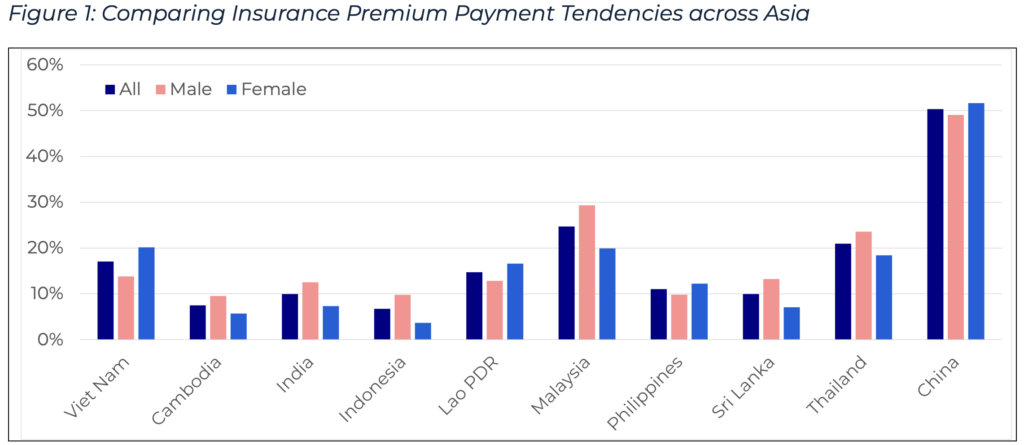

Income and employment influence insurance ownership

Several socioeconomic patterns are evident in the data.

Being in the workforce is consistently an indicator that insurance is more available and utilised. All countries report higher insurance take-up among workers. However, there is considerable variation. In Malaysia, 1/3rd of employed people reported having insurance, whereas this was just under 10 per cent in Cambodia and Indonesia. For those who are not in the workforce, some are still insured, although at rates somewhere between 2 per cent and 12 per cent.

Employed workers will have greater access to insurance through employment-related schemes and may also have more funds to pay for premiums. However, figures indicate that insurance solutions are possible and are being found for those not in the workforce (see Figure 2).

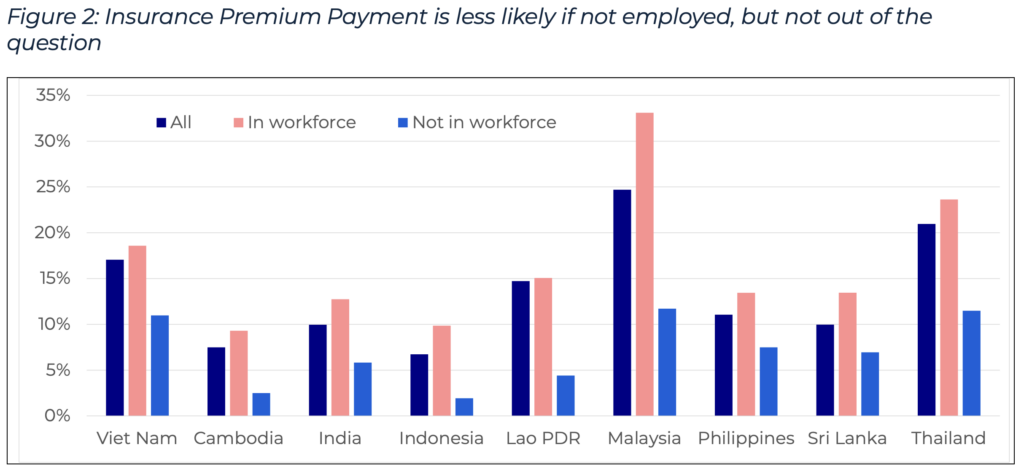

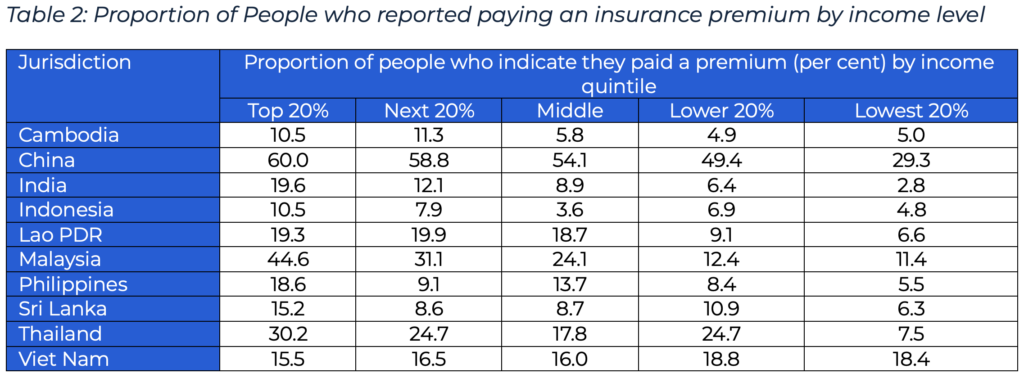

The trend against income levels is as expected, with insurance take-up generally increasing as relative incomes rise, but it also shows promising opportunities. Greater insurance uptake at higher income levels drops off as incomes fall, with the bottom 20% tending to be at least half as likely to have insurance as the top 20%, and, in some countries, the differences are more significant. This disparity is consistent with expectations. However, Viet Nam shows consistency across all income levels, and significant insurance take-up is also evident in Thailand and China in all quintiles except the very lowest. These countries suggest that initiatives can reach lower-income groups and at levels that would support mass market interventions.

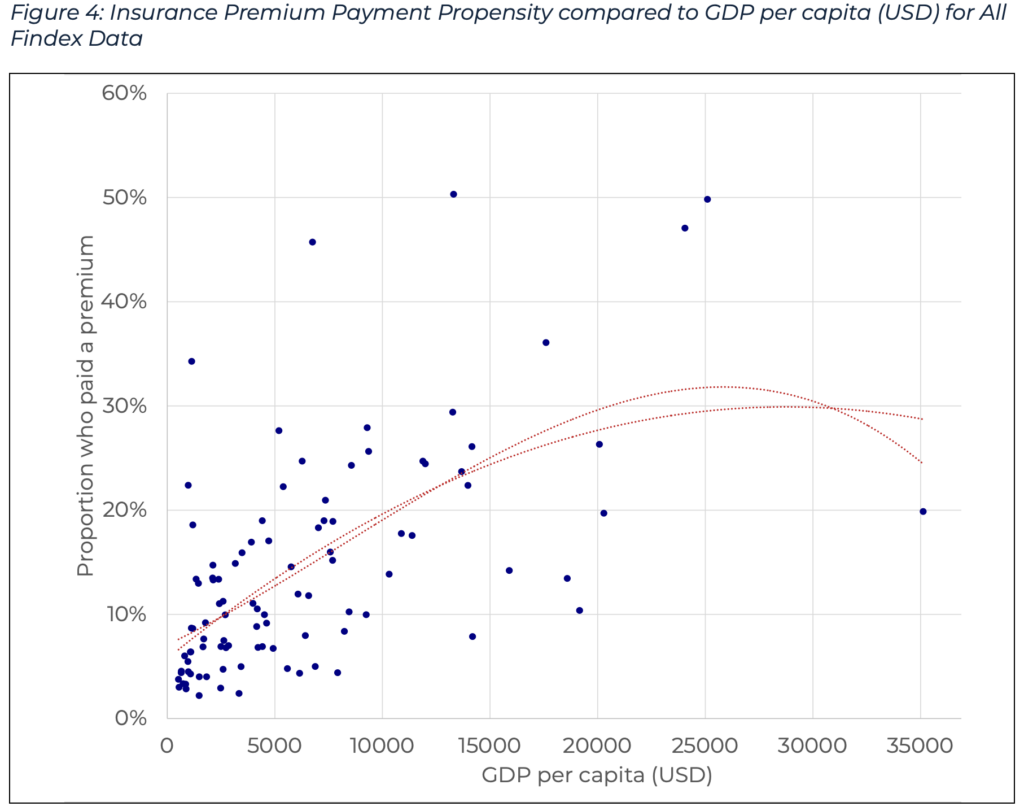

The usual “S-curve” hypothesis argues that insurance penetration, based on premiums to GDP, increases with income levels. Figure 3 shows that the Findex metric also tends to increase with income per capita, albeit with some variation. When compared to GDP per capita, Viet Nam, China and Malaysia all have a higher propensity than the regression line. Other countries in the region's data set fit well on the regression line.

Financial inclusion does not automatically translate into insurance inclusion

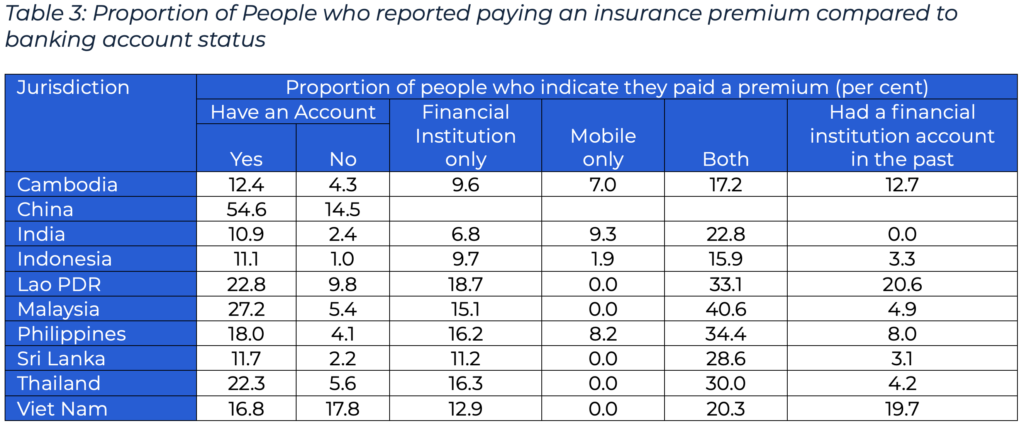

Having a transaction account has been viewed as the entry point to financial inclusion. This has often been interpreted to mean that insurance must follow efforts to make banking services more inclusive. This is true across the region, with the notable exception of Viet Nam (see Table 3).

Notably, people with both conventional financial institutional accounts and mobile accounts are more likely to have insurance. Having a mobile account only is little advantage in many countries except for India, the Philippines, and Cambodia and (to an extent) Indonesia. This suggests that mobile money providers are seen as more "core" in those jurisdictions for the underserved. Except for Viet Nam, Lao and Cambodia, those who had an account but are no longer account holders have a significantly lower likelihood of having made an insurance payment.

Where people did not have an account, it is might be expected that they do not have insurance for the same reasons. The picture shows some differences.

Rural communities often face significant challenges, and this is evident in Table 4 in Cambodia, China, India, Indonesia, and Malaysia. However, promisingly, rural communities have greater insurance utilisation in Laos, the Philippines, Sri Lanka, Thailand and Viet Nam.

Regardless of the reason people give for not having a bank account, they are also significantly less likely to be insured, even compared to all rural communities. Low trust in financial institutions for banking does not translate to insurance utilisation in the region, as most “low-trusting” clients have higher insurance usage than other reasons for being unbanked. Vietnam is, again, the exception across the board.

Geographic and demographic patterns, and financial engagement, show further insights

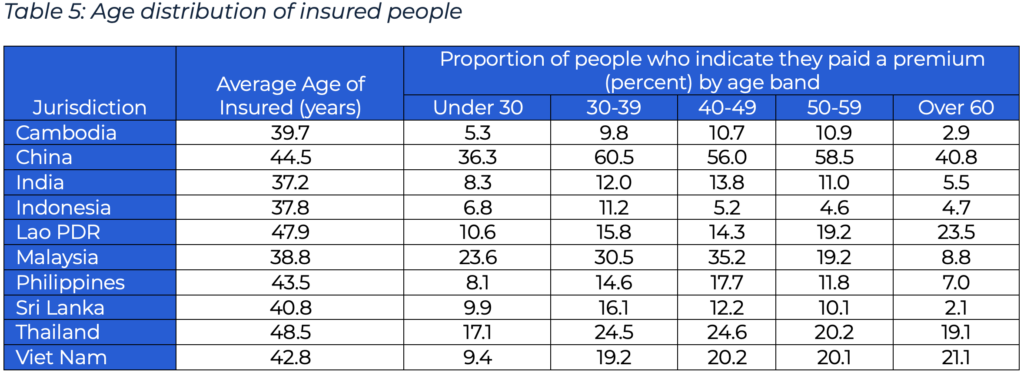

Information on the age profiles of insured people is valuable. The average age across countries varies, but it can be a feature of population age distributions. Within age groups, utilisation of insurance tends to be highest once people get to age 30 and, for older respondents, there is also a generally lower take-up (see Table 5). However, potential insurance solutions may vary considerably and contribute to the diverse results across countries. That said, this data point suggests that there is considerably deeper available data for insurance strategy and product development purposes in the data set, including by analysing age structure responses by sex or other characteristics.

Those who saved money in a financial institution tend to be twice as likely to have insurance as those who do not. For most countries, except Laos, borrowers are also more likely to have insurance than the country as a whole. Insurance ownership in Viet Nam is largely unchanged between borrowers and non-borrowers. With the exception of Viet Nam, entrepreneurial borrowers are more likely to have paid for insurance than those who borrow for medical emergencies. As those who borrow for medical emergencies also tend to be more likely to have insurance than the country average, this suggests that health insurance coverage may be generally less than needed, and that these clients have a familiarity with insurance. Unfortunately, it is not known whether they have health insurance or whether their insurance covers other risks

People who reported agricultural income also had above-average insurance take-up, except in Malaysia. This observation is encouraging for opportunities for insurance of agricultural risks, including parametric applications.

Implications for addressing protection gaps

The inclusion of insurance ownership in the Findex survey represents a significant step forward in understanding protection gaps at the individual level.

Several important implications emerge from this analysis.

- First, insurance coverage remains uneven and often limited, leaving large segments of populations financially exposed to shocks.

- Second, financial inclusion efforts, while important, do not automatically lead to financial protection through insurance. Expanding insurance coverage requires targeted efforts that address affordability, accessibility, and product design.

- Third, socioeconomic factors such as income, employment, savings behaviour, etc., continue to play an important role in determining insurance uptake.

At the same time, the data reveals promising signals. Examples across countries suggest that insurance solutions can reach lower-income and underserved populations, particularly when supported by targeted initiatives and appropriate distribution channels.

Looking ahead

The Findex dataset provides a rich source of information to support deeper analysis of insurance ownership across countries and population groups. This analysis is just a subset of the available analyses from this rich data set, highlighting the usefulness.

The addition of insurance ownership data to the Global Findex survey marks an important step toward better understanding protection gaps. Continued analysis of this data will help inform policies and market solutions that can strengthen resilience and improve financial protection across societies.

As a result, we encourage continued efforts to deepen the analysis of this data and for the World Bank to elaborate on more jurisdictions and greater granularity in their future surveys.